The Financial Mechanics of a Leveraged Buyout: Structure, Stakeholders, and Evaluation

By LBOstack

Explore the intricate financial mechanics of leveraged buyouts, including structure, stakeholders, and evaluation techniques for successful transactions.

The Financial Mechanics of a Leveraged Buyout: Structure, Stakeholders, and Evaluation

A leveraged buyout represents one of the most technically demanding transaction structures in private markets, combining disciplined capital allocation with a precise understanding of debt capacity, cash flow dynamics, and value creation levers. At its core, an LBO is an acquisition financed predominantly through borrowed funds, where the target company's existing assets and projected cash flows serve as both collateral for the debt and the primary mechanism for its repayment over time. For financial professionals working across private equity, corporate finance, and credit markets, understanding the mechanics that underpin these transactions is essential to evaluating deal risk, modelling returns, and structuring capital efficiently.

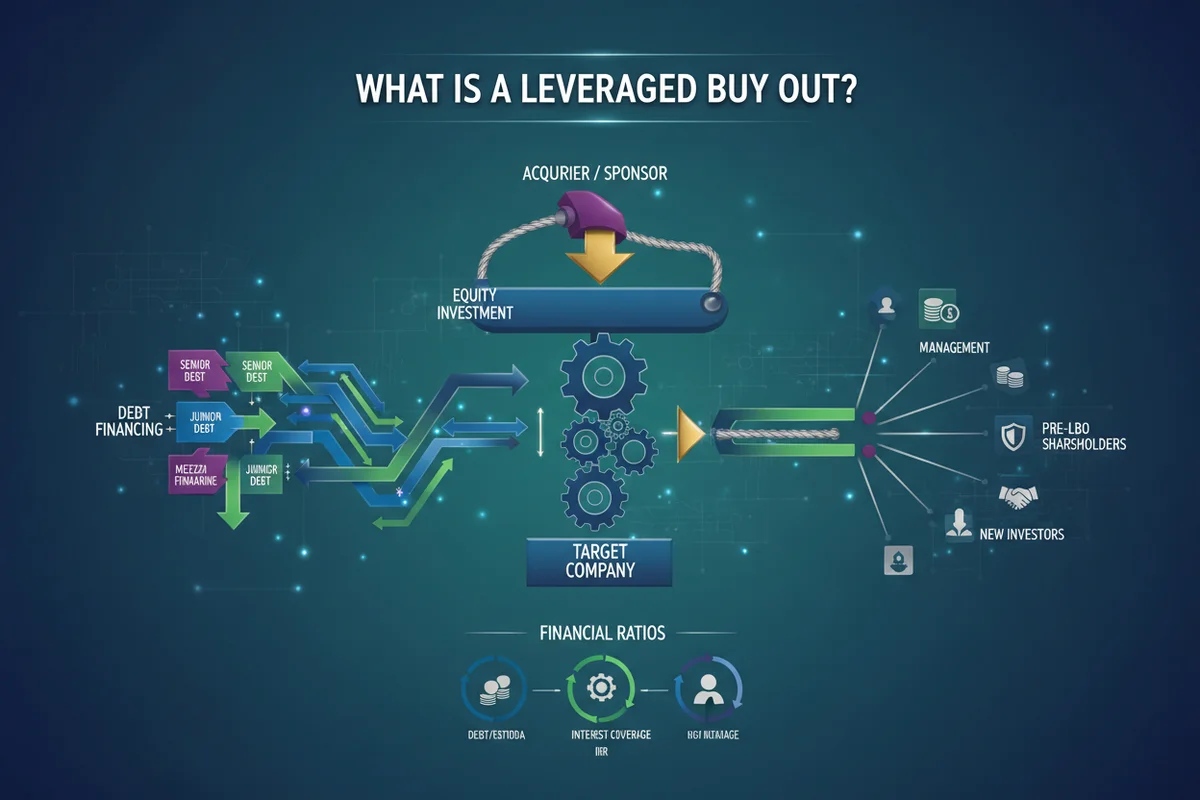

The Capital Structure of an LBO

The defining characteristic of any LBO is the proportion of debt relative to equity in the acquisition financing. In a typical transaction, debt constitutes between 60% and 80% of the total purchase price, with the remaining 20% to 40% funded through equity contributed by the acquiring private equity firm, according to LegalClarity. This ratio is not arbitrary but reflects a deliberate effort to amplify returns on invested equity by minimising the amount of capital the sponsor commits upfront while maximising the asset base over which gains are realised at exit.

Within the debt component, the capital stack is layered according to seniority and risk profile. Senior debt, which carries the highest repayment priority and is typically secured against the target's assets, is most commonly provided by commercial banks or direct lending funds. Below senior debt sits mezzanine or subordinated debt, which carries higher interest rates to compensate lenders for their junior position in the repayment waterfall and may include equity conversion features such as warrants or payment-in-kind interest mechanisms.

According to CT Acquisitions, a representative LBO financing structure in 2026 consists of approximately 35% to 45% senior debt, 10% to 15% mezzanine or subordinated debt, 30% to 40% sponsor equity, 10% to 15% seller financing, and between 0% and 15% in earn-out arrangements. This layered approach allows deal teams to optimise the weighted average cost of capital while maintaining sufficient flexibility in the debt structure to accommodate operational variability post-close.

Debt Pricing and Leverage Constraints in the Current Market

The cost and availability of leverage have shifted materially since the low-rate environment of 2021, when LBO transactions routinely carried leverage multiples of 6x to 7x EBITDA. In 2026, leverage caps have compressed to a range of 4x to 6x EBITDA, reflecting both tighter credit conditions and lender caution following a period of elevated base rates, according to CT Acquisitions. Senior debt pricing currently ranges from SOFR plus 450 to 650 basis points, translating to an all-in borrowing cost of approximately 9% to 11%, which has a meaningful effect on the returns achievable at a given entry multiple.

These dynamics require deal teams to be more precise in their underwriting assumptions, as higher debt servicing costs reduce the free cash flow available for debt amortisation and compress the equity return profile unless offset by stronger EBITDA growth or multiple expansion at exit.

Roles of Key Stakeholders

The private equity firm occupies the central role in an LBO, initiating the transaction, structuring the capital stack, contributing equity, and taking responsibility for the strategic direction of the business post-acquisition. The sponsor's equity contribution is typically deployed through a newly formed acquisition vehicle, often referred to as a special purpose vehicle or NewCo, which sits above the operating company in the legal structure and holds the debt obligations at the holdco level.

Lenders assess the target's ability to service debt through detailed credit analysis, focusing on the stability and predictability of operating cash flows, the quality of the asset base offered as security, and the headroom within financial covenants. Their appetite for a particular transaction is shaped by the industry sector, the cyclicality of earnings, and the existing leverage on the balance sheet prior to the acquisition.

Management teams occupy a distinct but important position in most LBO transactions. Senior executives are frequently invited to co-invest alongside the sponsor, acquiring equity stakes that vest over the holding period and align their financial incentives with those of the PE firm. This arrangement, often structured through a management equity plan, ensures that the people responsible for executing the operational strategy share meaningfully in the upside at exit while bearing some downside risk if performance targets are missed.

Financial Ratios Used to Evaluate LBOs

Three metrics dominate the analytical framework applied to LBO transactions. The debt-to-EBITDA ratio measures the total debt burden relative to operating earnings and serves as the primary indicator of leverage intensity. A ratio above 5x is generally considered aggressive in the current lending environment and will attract greater scrutiny from both lenders and rating agencies.

The interest coverage ratio, calculated as EBITDA divided by total interest expense, indicates whether the business generates sufficient operating earnings to meet its debt servicing obligations. A coverage ratio below 2x raises material concerns about the sustainability of the capital structure, particularly in a rising rate environment or during periods of earnings compression.

The internal rate of return is the metric through which private equity sponsors evaluate the attractiveness of a deal relative to their fund's return hurdle, typically set at 20% or above for buyout strategies. IRR is sensitive to entry multiple, leverage quantum, EBITDA growth assumptions, and exit timing, making it the central output of any LBO financial model and the figure around which investment committee debates are structured.

Illustrative Deal Examples

To illustrate how these mechanics operate in practice, consider a hypothetical mid-market transaction based on general market averages rather than a specific named deal. A PE firm acquires a business with EBITDA of AUD50m at an entry multiple of 8x, implying a total enterprise value of AUD400m. With leverage of 5x EBITDA, the debt component amounts to AUD250m and the equity contribution sits at AUD150m. At an all-in debt cost of 10%, annual interest expense is approximately AUD25m, leaving AUD25m of EBITDA available for debt amortisation, capital expenditure, and working capital requirements before any growth is achieved.

If the business grows EBITDA to AUD70m over a five-year holding period and exits at the same 8x multiple, the enterprise value at exit is AUD560m. After repaying the remaining debt balance, the equity return to the sponsor is materially amplified relative to what would have been achievable in an all-equity acquisition, demonstrating the fundamental return logic of leverage when cash flows are sufficient to service the debt.

Risks and Considerations

The amplification effect of leverage operates symmetrically, meaning that underperformance in cash flow generation can rapidly erode equity value and, in severe cases, trigger covenant breaches or restructuring events. Economic downturns, rising interest rates, and sector-specific disruptions can each impair the target's ability to service debt, as DataStudios notes, and the consequences of insufficient cash flow coverage are more severe in a highly leveraged structure than in a conservatively financed one.

For financial professionals building or auditing LBO models, the sensitivity of equity returns to changes in EBITDA, leverage costs, and exit multiples underscores the importance of rigorous scenario analysis and stress testing across a range of macroeconomic assumptions, ensuring that the investment thesis remains coherent even under conditions that deviate materially from the base case.